pigstand wrote:

拍照大不考慮維持一個緊急預備金?

這是個奇妙的問題。

你覺得應該是多少?

如果是半年的生活費,那當然是有。

如果是2%以上,那顯然是沒有。

我就是愛拍照 wrote:

根據之前對 LNC ...(恕刪)

我就是愛拍照 wrote:

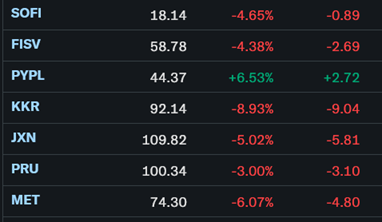

人壽保險股今天都倒..你前面看的JXN也倒..不過猜來猜去猜不到

Yield Curve Compression: Declining long-dated bond yields are compressing the yield curve, which is less advantageous for companies in the annuity and lending business

KKR & Co. Inc. (KKR) stock dropped significantly on Monday, February 23, 2026, falling over 8% due to a sharp price target downgrade by UBS Group (from

to

) and broader investor anxiety surrounding private-credit market liquidity. Increased bearish sentiment, with high put option activity ahead of upcoming earnings, further pressured the share price.

Positive Points

Jackson Financial Inc (NYSE:JXN) surpassed its financial targets for 2025, achieving record sales and distribution.

The company generated over $1 billion in free capital for the second consecutive year, supporting growth and capital return.

A strategic partnership with TPG was closed, expected to accelerate growth in spread-based business and provide future flexibility.

Retail annuity sales reached nearly $20 billion, the highest since 2019, with strong growth in RILA and fixed index annuities.

Jackson Financial Inc (NYSE:JXN) increased its quarterly dividend by nearly 13%, reflecting strong capital generation and shareholder returns.

Negative Points

Net income was impacted by annual assumption reviews and net hedge results, leading to a GAAP pretax loss.

Variable annuity net outflows remained elevated due to factors like an aging policyholder base and older sales vintages.

Higher-than-expected surrenders and market volatility posed challenges to capital generation.

The annual actuarial assumptions review resulted in a $360 million unfavorable impact due to updated policyholder behavior assumptions.

Despite strong sales, the company anticipates it will take a couple of years to achieve flat net flows due to ongoing variable annuity outflows.

Positive Points

F&G Annuities & Life Inc (NYSE:FG) achieved record assets under management (AUM) before flow reinsurance of $73.1 billion, up 12% over the previous year.

The company reported strong sales performance with $14.6 billion in gross sales for the year, including $9 billion from core products like indexed annuities and indexed universal life.

The investment portfolio is high-quality, with 97% of fixed maturities being investment grade, and credit-related impairments remaining stable at 8 basis points.

F&G's fee income from flow reinsurance grew by 37% to $56 million for the full year, indicating a successful shift towards more fee-based earnings.

The company maintained a strong capital position with an estimated risk-based capital ratio of approximately 430%, above their 400% target.

Negative Points

Alternative investment income underperformed, with a return of approximately 7% in the fourth quarter compared to the 10% long-term expected return.

The company faces potential headwinds in 2026 from fluctuating bond prepayments, which could impact variable investment income.

There is a risk of quarterly variability due to elevated annuity terminations, which could pressure near-term spreads.

F&G's stock is trading at a significant discount to book value, reflecting market concerns over credit losses despite a strong investment portfolio.

The company anticipates a decrease in AUM by $1.9 billion following the sale of its Bermuda-based legal entity, which could impact future earnings.

Positive Points

Lincoln National Corp (NYSE:LNC) reported a 31% year-over-year increase in adjusted operating income for the fourth quarter, marking the highest level in four years.

The company achieved its sixth consecutive quarter of year-over-year adjusted operating earnings growth, demonstrating strong performance across its business segments.

Annuity sales were strong in 2025, with total volumes up 25%, driven by a diversified product mix and strategic market positioning.

Group Protection segment delivered a record year with a 16% increase in full-year earnings, supported by premium growth and disciplined pricing.

The company has made significant progress in optimizing its operating model, creating a more efficient and scalable organization with sustained expense discipline.

Negative Points

The competitive landscape in the RILA market is intensifying, which may impact future sales growth in this segment.

Variable annuity net outflows continued, reflecting ongoing challenges in retaining business amidst higher equity markets.

Retirement Plan Services experienced net outflows of approximately $1 billion for the quarter, driven by participant withdrawals and plan terminations.

The company anticipates sequential pressure on annuities earnings in the first quarter of 2026 due to fewer fee days and resetting of favorable mortality experience.

Despite improvements, the Life Insurance segment still faces challenges in rebuilding sales momentum and optimizing free cash flow.